Introduction

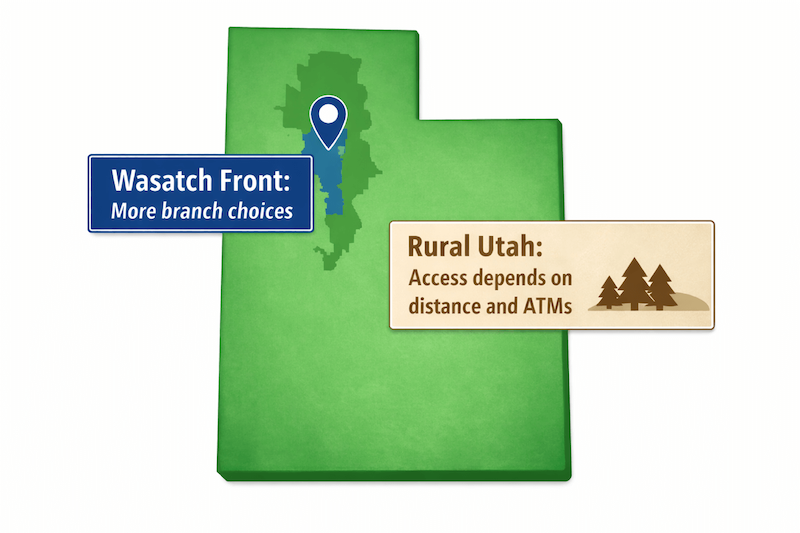

When deciding bank vs credit union in Utah, the right choice depends on how you bank day to day and where you live in the state. Along the Wasatch Front, you can often choose between large national banks, regional banks, and several credit unions within a short drive. In smaller cities and rural areas, the practical winner is often the institution with the most convenient branch access, reliable ATMs, and an app you can count on.

This question matters because Utah households and small businesses often need more than a basic checking account. Many people compare options when opening a first account, switching after moving within Utah, or choosing a lender for a car loan, mortgage, or small business financing. Banks and credit unions can both work well, but they are built differently. Those differences affect eligibility, fees, rates, customer service, and how lending decisions get made.

This Bank vs Credit Union in Utah guide explains what each type of institution is, how they compare, and which differences tend to matter most for Utah residents.

What Is a Bank?

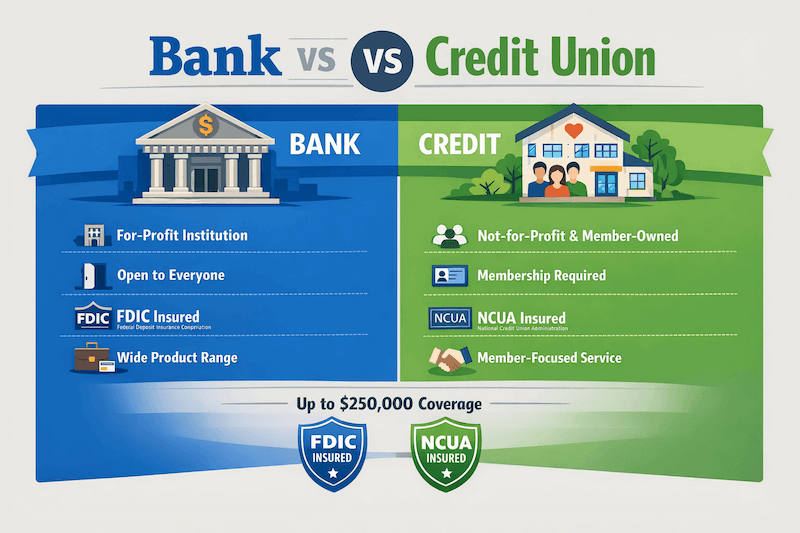

A bank is a for-profit financial institution that accepts deposits and makes loans. Banks typically offer checking and savings accounts, certificates of deposit, credit cards, mortgages, auto loans, and business services. Many banks are owned by shareholders, and their pricing and product decisions are usually designed to support profitability while staying competitive.

In Utah, you will find several types of banks:

-

National banks with large networks and standardized products across many states

-

Regional banks that operate across the Intermountain West and often combine scale with some local decision-making

-

Community banks that focus on relationship banking and may concentrate on specific Utah counties or business segments

-

Online banks that operate primarily through websites and mobile apps, often with limited or no physical branches and a stronger focus on digital tools and remote support

For many Utah residents, the main advantages of a bank are broad access, a wide menu of products, and tools that support more complex needs such as business banking, multiple account types, and services that work consistently when traveling outside the state.

In the bank vs credit union in Utah decision, banks often stand out for product breadth and open access.

Read our guide for the Best Banks in Utah.

What Is a Credit Union?

A credit union is a member-owned financial cooperative that accepts deposits and makes loans. Instead of being owned by shareholders, a credit union is owned by the people who use it. When you open an account, you become a member, and the institution’s goal is generally to serve members rather than maximize profit.

Credit unions in Utah commonly offer the same core products most households need, including checking and savings accounts, certificates of deposit, credit cards, auto loans, and mortgages. Many also offer business accounts and small business loans, though the product selection can be narrower than what you might see at a large bank.

The biggest difference is eligibility. Credit unions have membership rules called a field of membership. In Utah, that eligibility is often based on where you live, where you work, a family connection, or membership in a participating organization. Many Utah credit unions make membership easy for residents through broad community eligibility, but it is still worth confirming before you start an application or move direct deposits.

For Utah residents, credit unions are often chosen for member-focused service, competitive pricing on everyday accounts, and a stronger community presence in certain regions of the state.

In the bank vs credit union in Utah comparison, credit unions are often chosen for member ownership and community-rooted service.

Read our guide for the Best Credit Unions in Utah.

Key Differences That Matter in Utah

Bank vs Credit Union in Utah

| Factor | Banks | Credit Unions |

|---|---|---|

| Ownership | For-profit | Member-owned |

| Access | Open to most | Membership required |

| Utah branches | Varies by bank | Often regional strength |

| Fees | Varies by account | Often member-focused |

| Rates | Varies by borrower | Often competitive |

| Products | Wider menu | Core products strongest |

| Digital | Often robust | Varies widely |

| Best for | Breadth + scale | Value + community |

When comparing bank vs credit union in Utah, the differences that matter most are usually practical: who can join, where you can bank in person, how fees are structured, how competitive borrowing can be, and how strong the digital experience is.

Ownership structure

Banks are generally owned by shareholders and operate for profit. Credit unions are owned by members and typically operate with a not-for-profit model. In daily life, this can influence fees, loan rates, and account policies.

In Utah, ownership structure can also affect how local decision-making feels. Some Utah-based banks and many credit unions emphasize local relationships and local lending knowledge, while large national banks may rely more on standardized underwriting and centralized policies. The right fit depends on whether you value a member-owned model or prefer a broader, standardized banking platform.

Membership vs open access

Most banks are open to anyone who meets standard identity and account requirements. Credit unions require eligibility through membership rules. Many Utah credit unions serve broad communities, which makes joining simple for many residents, but the rules still vary.

This matters most when you want to open an account quickly, add a family member, or keep multiple accounts in one place. If you prefer open access with minimal eligibility steps, a bank may feel easier. If you qualify for a credit union that fits your needs, membership can be a straightforward tradeoff for a more member-focused structure.

Bank vs Credit Union in Utah access

Branch presence in Utah

Branch access can still matter in nowadays, especially if you deposit cash, need cashier’s checks, want in-person problem-solving, or prefer face-to-face service. In Utah, branch convenience is highly regional. The Wasatch Front typically has the most options, while other areas may have fewer branches and longer drives.

Credit unions may have strong coverage in specific counties or cities, and some use shared branching networks that expand access beyond their own locations. Banks may offer broader in-state coverage if they have many Utah branches, and national banks may provide access when you travel out of state. For most people, the best branch network is the one that matches where you live and work, not the one that is largest on paper.

Fees and rates

Both banks and credit unions charge fees in certain situations and both can offer competitive rates. The difference is often in how pricing is structured:

-

Credit unions often compete well on everyday value, including fewer monthly charges, lower minimums, and competitive loan rates for members.

-

Banks may offer strong promotions, relationship pricing, and broader premium tiers, especially if you keep higher balances or bundle multiple services.

For Utah residents, the right comparison is not category versus category. It is product versus product. Compare the checking account fee schedule, the conditions that trigger fees, the interest rate on the savings option you would actually use, and the loan rates that match your credit profile and term.

Technology and digital banking

Digital banking quality varies widely across both banks and credit unions. Some credit unions have modern apps and strong online tools. Some have fewer features or slower updates. Banks often invest heavily in technology, but that does not guarantee a better experience when issues come up.

If you rarely visit a branch, digital quality becomes a primary deciding factor. Features that often matter in real life include mobile deposit reliability, external account transfers, real-time alerts, card controls, fraud handling, and customer support availability outside business hours. When comparing bank vs credit union in Utah, focus less on the logo and more on the tools you will use every week.

Deposit insurance in Utah: FDIC vs NCUA

Most banks are insured by the FDIC (Federal Deposit Insurance Corporation), and most credit unions are insured by the NCUA (National Credit Union Administration). In both cases, eligible deposits are typically covered up to $250,000 per depositor, per institution, per ownership category. If you want a fuller explanation of how this protection works, see What FDIC Insurance Means for Utah Bank Customers and What NCUA Insurance Means for Utah Credit Union Members.

When a Bank Might Be a Better Fit

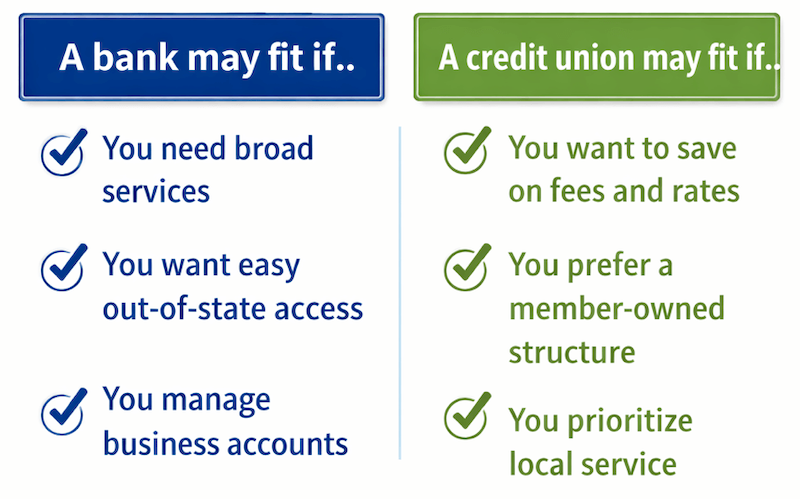

When comparing bank vs credit union in Utah, a bank can be the better choice if you prioritize access, product breadth, and consistency across locations.

You want broader product options in one place

Banks often offer a wider lineup of services under one login, especially for business banking, credit cards, and specialized lending. If you want checking, savings, a credit card, a mortgage, and business services all bundled together, a bank may be simpler.

You travel often or want out-of-state access

If you spend time outside Utah for work, school, or family, a bank with a larger footprint can make it easier to find branches and ATMs and get help in person when you need it.

You rely on advanced digital tools

Many banks invest heavily in digital banking features like transfers, alerts, card controls, and integrated tools for budgeting and account management. If you bank mostly on your phone and expect a highly polished app experience, a bank may be a safer bet, depending on the institution.

You want open access without membership steps

Banks are generally open to anyone who meets standard requirements. If you prefer a straightforward setup without eligibility rules, a bank can be easier for opening accounts quickly or adding household members.

You need business services or more complex support

Utah’s small business community often needs tools like ACH payments, wires, merchant services, and cash management options. Many banks are better equipped for these needs, especially as a business grows.

When a Credit Union Might Be a Better Fit

When comparing bank vs credit union in Utah, a credit union can be the better choice if you want member-focused pricing, local service, and a simpler everyday banking relationship.

You care most about everyday value

Credit unions often compete well on day-to-day costs, especially if you want a straightforward checking account, predictable fees, and a relationship that does not depend on keeping high balances.

You prefer a member-owned model

If you like the idea of banking with an institution that is owned by its members, a credit union can align better with your values. For many people, this also translates into a service style that feels more personal.

You want local lending context

Many credit unions emphasize relationship lending and local decision-making. In Utah, that can matter when you want a lender that understands local housing conditions, regional employment patterns, or the realities of living in different parts of the state.

You mostly need core products

If your needs are checking, savings, an auto loan, and a mortgage, many credit unions cover these well. You may not need the broader product menu that comes with a large bank.

You want strong community presence in your area

Some credit unions have especially strong coverage in specific Utah counties and cities. If your local credit union has convenient branches, a good ATM setup, and reliable support, it can be an excellent long-term fit.

Bank vs Credit Union in Utah

Final Considerations for Utah Residents

Before you decide bank vs credit union in Utah, narrow the choice to what will affect your finances and your routine the most.

Start with your real banking habits

Write down what you actually do in a typical month:

-

Do you need to deposit cash?

-

Do you need cashier’s checks or other branch services?

-

How often do you use ATMs, and where?

-

Are you likely to apply for a car loan or mortgage soon?

-

Do you want business banking now or later?

-

Do you manage everything through a phone app?

The best institution is usually the one that removes friction from the tasks you do most.

Compare the exact accounts you would open

Do not compare categories. Compare products. Review the fee schedule for the checking account you plan to use and look for the fees people actually hit: monthly charges, overdraft policies, out-of-network ATM costs, and replacement card policies. If you keep a savings balance, compare the savings option you would actually use, not an account tier you will not qualify for. Once you have decided an account to open, read our guide How to Open a Bank Account in Utah.

Separate “daily banking” from “best loan”

Many Utah residents use one institution for daily banking and shop separately for major loans. That can be a smart approach if your goal is the best overall fit, not an all-in-one relationship. It also gives you flexibility if you move within Utah or your needs change.

Evaluate digital support and problem resolution

When something goes wrong, support matters more than features. Check whether you can reach a person easily, whether support hours match your schedule, and whether disputes and fraud issues are handled clearly. This matters even more if you live far from a branch or travel frequently.

Choose for where you live in Utah

If you are on the Wasatch Front, you usually have enough branch density to choose based on product fit and service style. If you are outside major metro areas, branch location and ATM access can outweigh small differences in rates or perks. In that case, the best choice is often the one that is reliably accessible where you already spend your time.

How to decide which is better for you in Utah

If you prefer nationwide access, larger branch networks, and a broader range of products, a bank may be the better fit. You can compare your options in Best Banks in Utah. If you prefer a more local, member-focused approach and want to explore strong credit union options across the state, start with Best Credit Unions in Utah.

Conclusion

There is no universal winner in the bank vs credit union in Utah decision. Banks can be a better fit when you want broad product options, open access, and consistent service across locations. Credit unions can be a better fit when you want a member-owned model, strong everyday value, and a more community-rooted approach.

If you compare the specific accounts you will use, confirm branch and ATM access where you live, and prioritize the digital tools you rely on every week, you can choose with confidence based on fit rather than assumptions.