Introduction

Starting a business in Utah costs money before it makes money. Even small businesses usually have early expenses like supplies, equipment, insurance, software, or marketing. Some businesses also have rent, utilities, or payroll. If you do not plan for these costs, you can run out of money quickly, even if customers like what you sell.

This financial checklist for starting a business in Utah is about getting your money ready before you launch. It focuses on the basics: how much money you need to start, how long your savings can cover expenses, how to keep business money separate, how to set money aside for taxes, how to track income and expenses, how you will get paid, and how to plan for risks like emergencies and insurance.

It does not explain how to register a business or choose a legal structure. The goal is to help you start with a clear budget and simple systems so you can avoid common money problems in the first few months.

Table of Content

- Estimate Your Startup Costs

- Separate Personal and Business Finances

- Prepare to Open a Business Bank Account

- Set Up a Tax Money System

- Choose a Bookkeeping System

- Plan for Payment Processing

- Understand Insurance and Risk Planning

- Think About Funding and Credit

- Final Financial Readiness Checklist

- Conclusion

Estimate Your Startup Costs

Before you launch, you need a clear idea of how much money it will take to start and how much it will take to keep the business running each month. This is a key part of a financial checklist for starting a business in Utah because it tells you whether your plan is affordable right now.

You can use the SBA’s startup cost guide as a reference.

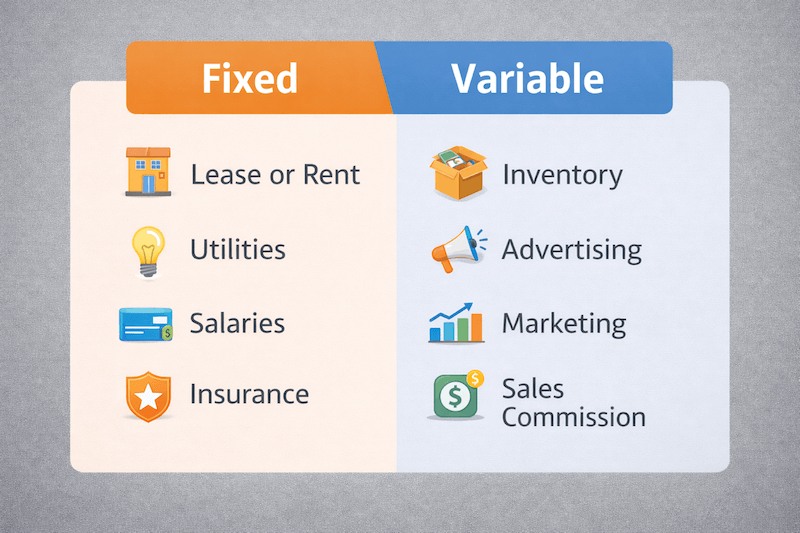

One-Time Costs vs Monthly Costs

Start by separating costs into 2 simple groups.

One-time costs (usually paid before opening or early on):

- Equipment and tools

- A computer, phone, or printer

- Initial supplies

- First inventory order

- Website setup or branding work

- Deposits (like rent or utilities)

Monthly costs (repeat every month):

- Rent (if you have it)

- Insurance

- Internet and phone

- Software subscriptions

- Advertising or marketing

- Inventory reorders

- Delivery, shipping, or mileage costs

- Payments to helpers or contractors

Write your best estimate for each item. If you are unsure, use a higher number so you are not surprised later.

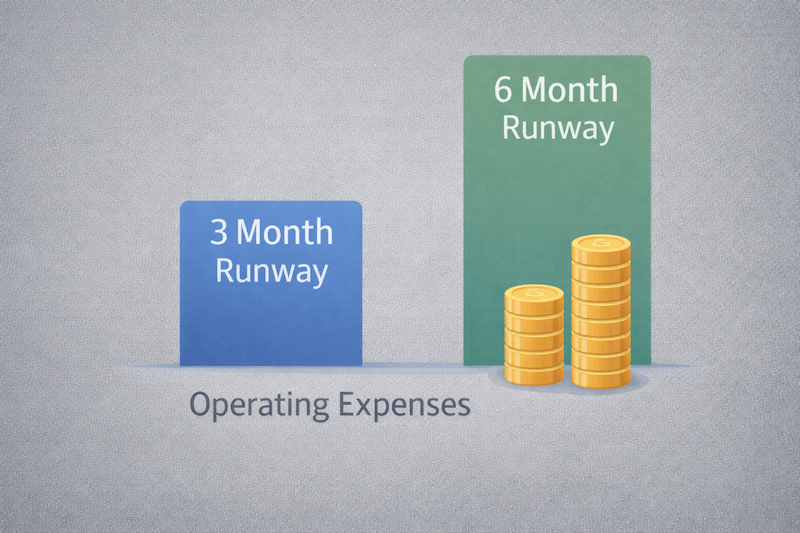

How Many Months Can You Cover?

Next, calculate how many months your savings can cover your monthly costs.

Ask yourself:

If I made no money for a few months, how long could I still pay the business bills?

Example:

- You have $15,000 saved for the business

- Your monthly costs are about $3,000

15,000 ÷ 3,000 = 5

You can cover about 5 months.

Many people aim for at least 3 months. Having closer to 6 months gives you more breathing room if sales start slow.

Add a Cash Buffer

New businesses usually face surprises:

- You need to replace something

- A customer pays late

- A slow month happens

- A cost is higher than expected

Plan for this by adding extra money on top of your estimates. Even a small buffer can prevent a short-term cash problem from turning into a major issue.

Separate Personal and Business Finances

One of the easiest ways to create money problems in a new business is to mix business spending with personal spending. Even if your business is small, keeping the money separate helps you stay organized and avoid mistakes.

Why Separation Matters

When your business money is separate, you can answer basic questions quickly:

- Is the business making money or losing money?

- How much can the business afford to spend this month?

- How much should you set aside for taxes?

It also makes bookkeeping simpler because your business transactions are all in one place.

If you need to open a personal checking account, check our guide Best Checking Accounts in Utah.

If you need to open a busienss account, check our guideBest Business Checking Accounts in Utah.

Risks of Mixing Funds

When everything runs through your personal account, common problems show up fast:

- You forget which purchases were for the business

- You miss expenses that should be tracked

- You spend business money on personal bills without noticing

- It becomes harder to understand your true monthly costs

Mixing money also makes it harder to get help later. If you ever hire a bookkeeper or accountant, messy records cost more time and more money to clean up.

Simple Planning for a Basic Setup

You do not need a complicated system to start. You need a clear plan.

At minimum, plan for:

- 1 business checking account for income and expenses

- 1 business savings account for taxes (and later, for reserves)

- A clear rule for owner pay (how you move money from business to personal)

Even if you start with small amounts, separating the money early makes everything else in this financial checklist for starting a business in Utah easier to manage.

Prepare to Open a Business Bank Account

A business bank account is a key part of any financial checklist for starting a business in Utah because it keeps your business money separate and makes income and expenses easier to track. It also helps you start with clean records from day 1. It also helps to understand what documents you need to open a business bank account in Utah before you start gathering everything.

Check our guide for Best Business Checking Accounts in Utah.

If you want a bigger picture view of local institutions, see:

What Financial Documents and Details to Have Ready

You do not need a long folder of paperwork for this checklist, but you should have your financial details clear before you apply so you choose the right account.

Have these ready:

- Your starting deposit amount (how much you will put in the account right away)

- Your expected monthly activity (how many deposits and payments you expect)

- How you expect to get paid (card payments, bank transfers, checks, cash)

- Your monthly budget estimate (rough monthly spending so you can avoid fee surprises)

The goal is to avoid opening an account that looks free at first but becomes expensive once you start using it.

Choosing Between a Bank and a Credit Union

Both banks and credit unions can work for business banking. The best choice depends on how you plan to use the account.

In general:

- A bank may be a better fit if you want a larger branch network, more business account options, or more business lending products later.

- A credit union may be a better fit if you want lower fees, a simpler relationship, or a more local experience.

For a full comparison, see:

Plan for Fees and Limits

Before you choose an account, look at these items:

- Monthly service fee (and how to avoid it)

- Minimum balance requirements

- Number of transactions included per month

- Cash deposit limits (if you handle cash)

- Wire or transfer fees (if you pay vendors that way)

Even small fees add up. The right account depends on your expected activity, not just the name of the institution.

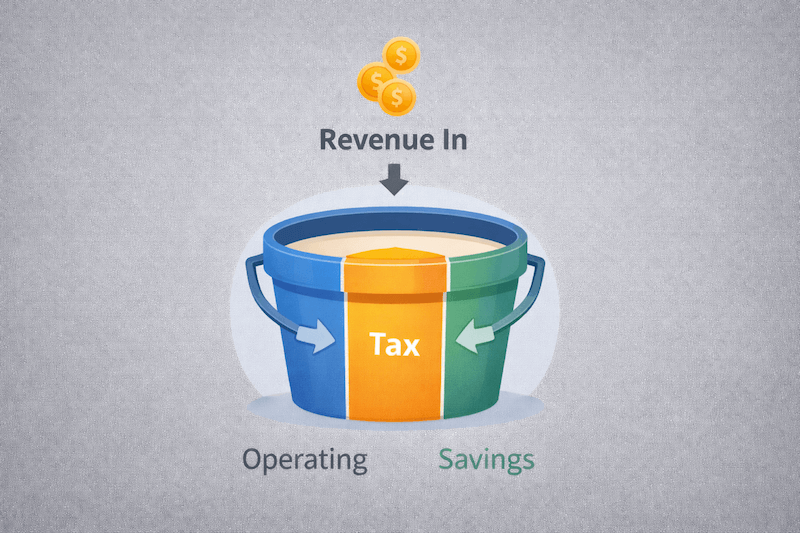

Set Up a Tax Money System

When you start a business, taxes do not get taken out automatically the way they do with a regular paycheck. That means it is easy to spend money that was never really yours to spend. A simple “set-aside” system helps you avoid that problem.

Helpful link: IRS Small Business and Self-Employed Tax Center

This is an important part of a financial checklist for starting a business in Utah because tax stress often comes from one issue: the money was not separated early.

Why You Need a Set-Aside System

If you wait until tax time to figure it out, you may realize you owe more than what is left in your account. Even if the business is doing well, that can cause a cash squeeze.

Setting money aside regularly keeps taxes from becoming a surprise bill.

Simple “Split Every Payment” Approach

A basic method is:

Whenever your business gets paid, move a portion of that money into a separate savings account and leave it there.

Helpful Link: IRS Estimated Taxes Overview

You do not need a perfect number on day 1. What matters is the habit:

- money comes in

- you move part of it out right away

- you do not spend that tax money

If you want to keep it simple, pick a percentage and use it every time. You can adjust later when you have more real numbers.

Use a Dedicated Savings Bucket

Open a separate savings account and label it “Tax.”

Then set a rule:

-

After every deposit, transfer your tax set-aside amount into that account.

This keeps your main checking balance more honest. It helps you avoid looking at your checking account and thinking you have more spending money than you really do.

Choose a Bookkeeping System

Bookkeeping is a core part of a financial checklist for starting a business in Utah because it helps you understand where your money is going. You do not need an advanced system to start, but you do need a consistent one. If you wait until months later, it is harder to fix.

Basic Tracking Categories

Start with a short list of categories that covers most businesses. You can add more later.

Common categories include:

- Income

- Supplies or inventory

- Marketing and advertising

- Software and subscriptions

- Rent or workspace

- Insurance

- Travel or mileage

- Professional services

- Equipment

- Taxes set aside (transfers to savings)

Keep categories simple enough that you will actually use them.

A Monthly Money Check-In

Once per month, do a short review:

- Make sure all income and expenses are recorded

- Check your business account balance

- Confirm you moved money into your tax savings account

- Review any unpaid invoices or bills

This keeps small issues from turning into bigger ones.

Keep Receipts in One Place

Pick one place where receipts and invoices will live. The goal is that you can find them later without searching through texts, emails, and photos.

Simple options:

- A folder in cloud storage

- A dedicated email label

- A bookkeeping app that stores attachments

If you handle receipts as you go, you avoid a pile-up at the end of the year.

Plan for Payment Processing

How you get paid affects your cash flow. Some payment methods are fast. Others take time. Some include fees that reduce what you keep. This section of the financial checklist for starting a business in Utah helps you avoid surprises after you start selling.

Decide How You Will Get Paid

Think about how customers will pay you in real life.

Common options:

- Debit and credit cards

- Online invoices with card or bank payment

- Bank transfers

- Checks

- Cash

You may use more than one. The key is to choose methods that match your customers and your pricing.

Know the Fees Before You Set Prices

Card payments and online payment services usually charge fees. Those fees reduce your profit on every sale.

Before you set your prices, make sure you understand:

- whether the fee is a percentage, a flat amount, or both

- whether you pay extra for refunds, chargebacks, or instant transfers

You do not need to memorize fee tables. You just need to remember that not every dollar a customer pays will land in your account.

Plan for Timing Delays

Some payment methods do not show up in your bank account immediately. That matters when you have bills due.

Ask:

- How quickly will money hit my bank account after a customer pays?

- What happens on weekends or holidays?

- If I issue a refund, how does that affect my balance?

Build your budget assuming some delays. That helps you avoid being short on cash even in a month with good sales.

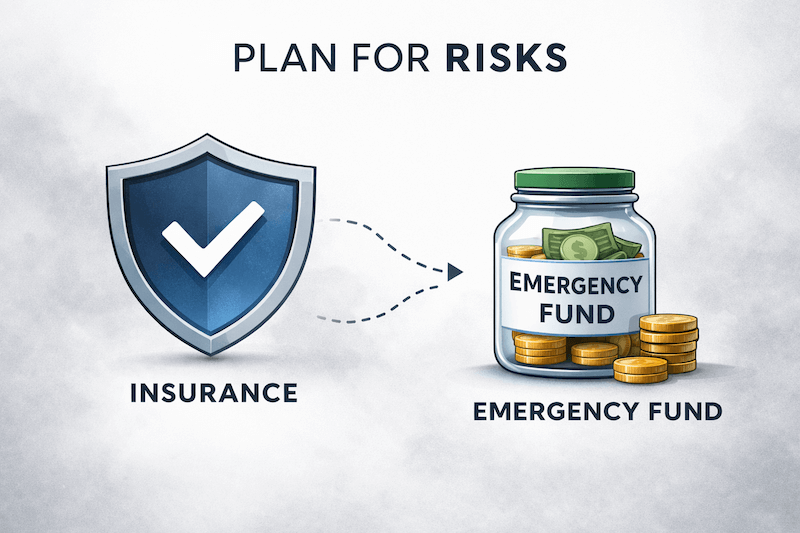

Understand Insurance and Risk Planning

Every business faces some level of risk. Even small businesses can face unexpected costs. Planning for those risks is part of a responsible financial checklist for starting a business in Utah.

Insurance and emergency savings are not about fear. They are about stability.

Budget for Insurance

Before you launch, get an idea of what insurance may cost for your type of business.

Common types include:

- General liability insurance

- Professional liability insurance

- Commercial auto insurance (if you use a vehicle for business)

- Property coverage (if you own equipment or inventory)

You do not need to buy every type of coverage immediately. But you should request quotes so you can include those costs in your monthly budget.

Insurance is a regular expense. If you ignore it in your planning, it can feel like a surprise later.

Build a Business Emergency Fund

In addition to covering monthly expenses, it helps to keep extra money set aside for unexpected problems.

Examples:

- Equipment breaks

- A large client cancels

- A repair is needed

- A slow month happens

This emergency money should stay in the business, not mixed with personal savings. Even a small reserve gives you options. Without it, a short-term problem can turn into a larger financial issue.

Insurance and emergency savings are often overlooked in a financial checklist for starting a business in Utah, but they protect you from setbacks. Planning for risk does not guarantee smooth growth. It simply reduces the chance that one setback forces you to stop operating.

Think About Funding and Credit

Before you launch, decide how you will pay for the business and what you will do if you need extra money later. This part of the financial checklist for starting a business in Utah helps you avoid taking on debt too early or relying on money you do not actually have.

Personal Money vs Outside Money

Most new businesses start with personal money:

- savings

- income from a job

- help from family

- money set aside over time

Personal money can be simple because there is no lender and no payment due each month. The downside is that you are taking the risk personally.

Outside money can include:

- a loan

- a line of credit

- a credit card

- an investor

Outside money can help you move faster, but it also adds pressure because payments still happen even in slow months.

Understand What Debt Does to Your Monthly Budget

If you borrow money, your monthly expenses usually go up.

That matters because you need enough cash each month to cover:

- normal business costs

- your personal living costs

- and the new payment

If your business is not earning steady income yet, debt can create stress and reduce flexibility.

Keep Credit Use Simple Early On

If you plan to use credit, start with clear rules:

- Only use credit for business expenses

- Track every purchase

- Pay attention to the payment due dates

- Avoid using credit to cover basic bills month after month

The goal is to avoid turning short-term cash problems into long-term debt.

If you are not sure what you will need, it is often better to start smaller, keep monthly costs low, and build up as your income becomes more predictable.

Final Financial Readiness Checklist

Before you launch, review this list. A complete financial checklist for starting a business in Utah should feel clear and manageable, not rushed or uncertain.

Startup Costs

- Listed all one-time costs

- Estimated realistic monthly costs

- Added extra money for unexpected expenses

Months Covered

- Calculated how many months your savings can cover expenses

- Confirmed you have at least 3 months covered

- Aimed for closer to 6 months if possible

Banking

- Planned to open a separate business checking account

- Reviewed account fees and limits

- Decided whether a bank or credit union fits your needs

Helpful comparisons:

You can compare the different financial institutions with our guides Best Banks in Utah and Best Credit Unions in Utah. Or the Best Checking Accounts in Utah.

Taxes

- Chosen a simple percentage to set aside

- Opened a separate savings account for taxes

- Created a habit to move money after each deposit

Bookkeeping

- Chosen a basic tracking method

- Created simple income and expense categories

- Scheduled a monthly money review

- Set up a place to store receipts

Payments

- Decided how customers will pay

- Reviewed payment processing fees

- Understood how long deposits take

Insurance and Risk

- Requested insurance quotes

- Added insurance to monthly cost estimates

- Set aside extra money for emergencies

Funding

- Decided how you will fund the business

- Reviewed the impact of any debt on monthly costs

- Avoided borrowing more than needed

Conclusion

Financial preparation does not guarantee success, but it reduces avoidable mistakes. When you understand your costs, separate your money, plan for taxes, track your expenses, and prepare for slow months, you give your business a stronger start.

Taking time to complete this financial checklist for starting a business in Utah helps you launch with structure instead of guesswork.