Central Bank Utah: Overview

![]() Central Bank Utah has a history that goes back more than 132 years. It was founded on October 17, 1891 by Milan Packard as the Springville Banking Company. In 1966, the Springville Banking Company merged with the State Bank of Provo to form Central Bank and Trust. This merger brought together two of Utah County’s oldest banks and strengthened their lending capacity and financial stability. Central Bank was also a pioneer in the state, becoming the first bank in Utah to qualify for FDIC deposit insurance.

Central Bank Utah has a history that goes back more than 132 years. It was founded on October 17, 1891 by Milan Packard as the Springville Banking Company. In 1966, the Springville Banking Company merged with the State Bank of Provo to form Central Bank and Trust. This merger brought together two of Utah County’s oldest banks and strengthened their lending capacity and financial stability. Central Bank was also a pioneer in the state, becoming the first bank in Utah to qualify for FDIC deposit insurance.

Central Bank Utah: Corporate Office

75 N University Ave.

Provo, UT 84601

Cities where Central Bank Utah operates include:

American Fork, Lehi (2), Mapleton, Orem, Payson, Pleasant Grove, Provo (2), Saratoga Springs, Spanish Fork, Springville

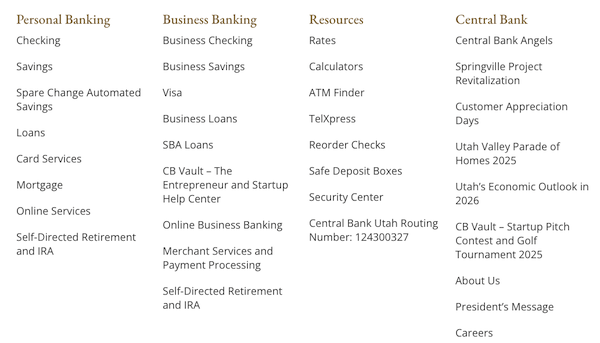

Central Bank Consumer Products and Services

cbutah.com | Products & Services

Central Bank Utah offers a full set of everyday banking products and services for individuals and local businesses, with a focus on core deposit accounts and lending. Customers can typically expect checking and savings options, certificates of deposit, and borrowing solutions like personal loans and home financing, supported by digital tools such as online banking, mobile banking, and bill pay. Below, we’ll start with checking accounts, since that’s usually the foundation for direct deposit, debit card access, and day-to-day money management.

Central Bank Utah Checking Accounts

Free Checking

A basic everyday checking option designed for simple banking like deposits, payments, and debit card spending. It’s positioned for people who want a straightforward account without added complexity.

62+ Free Interest Checking

A checking option for customers 62+ that combines everyday account access with the ability to earn interest. It’s designed for people who keep a consistent balance and want their checking to do a little more than just handle transactions.

Shared Features

Both accounts include online and mobile banking, mobile deposit, and everyday payment tools like bill pay and Zelle®, plus a debit card and ATM access. They also offer basic account management like alerts and monthly statements, with optional overdraft protection, and they typically require a $50 opening deposit.

Savings Accounts

Statement Savings

A traditional savings account designed for building an emergency fund or saving for near-term goals, with simple access and FDIC insurance. It’s a straightforward option if you want a separate place to keep savings outside of checking.

High Yield Money Market Account

A higher-earning savings-style account that’s designed for people who keep a larger balance and want more earning potential than a basic savings account. It also offers some transaction flexibility, but it’s still meant primarily for saving rather than everyday spending.

YOUth Smart Savings (Ages 0–18)

A kids savings account designed to help families teach saving early, with features aimed at encouraging good habits. It’s built specifically for minors and positioned as a “starter” savings option for children and teens.

Spare Change Automated Savings (Round-Up Tool)

Central Bank Utah offers an optional “Spare Change” tool that rounds up debit card purchases to the nearest dollar and automatically moves the difference into a linked savings or money market account. It’s designed to help customers save passively through everyday spending, using online banking or the mobile app to enroll and manage it.

Certificates of Deposit

A fixed-term savings option designed for longer-term goals, where your rate is tied to the term you choose. Central Bank CDs are available in multiple term ranges, including 60 days to 5 months, 6 to 11 months, 12 to 23 months, 24 to 35 months, 36 to 47 months, 48 to 59 months, and 60 months. Rates vary by term and deposit amount, and CDs are FDIC-insured up to $250,000, with early withdrawal penalties if you take funds out before maturity.

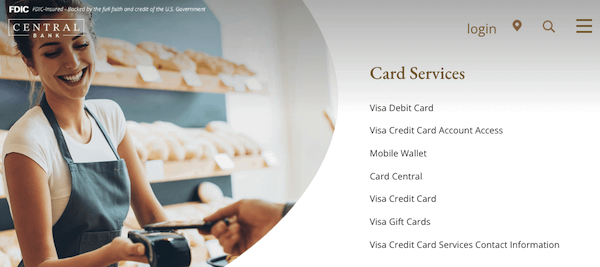

Central Bank Credit Cards

cbutah.com | Credit Card Services

Central Bank Utah keeps its credit card lineup simple: it offers 1 personal credit card, supported by a set of credit card services inside its digital banking experience. Instead of multiple card tiers, the focus is on making it easy to apply, manage your card, and control everyday settings through online and mobile tools.

Central Bank Visa Credit Card

Central Bank’s Visa credit card is its single consumer card option, designed for everyday purchases and managed through the bank’s credit card services and digital tools. It’s positioned as a straightforward local-bank card for customers who prefer to keep banking and card management in one place.

Personal Loans

cbutah.com | Personal Loans

Personal Loans

Central Bank Utah offers personal loans designed for borrowers who want local servicing and a community-bank lending experience. These loans are typically used for planned expenses, consolidating balances, or unexpected costs.

Auto Loans

Auto loans are available for customers who want to finance a vehicle through the bank instead of relying only on dealership financing. This option is positioned for everyday transportation needs with local support.

Recreational Vehicle Loans

Central Bank also finances recreational purchases such as RVs and similar categories. This is aimed at borrowers who want to keep their recreational lending with the same institution where they bank.

Personal Line of Credit

A personal line of credit provides flexible access to funds over time instead of a one-time lump sum. It can be useful for uneven expenses or projects that come in phases.

CD or Savings Secured Loans

If you have a Central Bank CD or savings account, you may be able to use it as collateral for a loan. This is often used to build credit or pursue more favorable terms while keeping funds on deposit.

Central Bank Mortgages

Conventional Mortgage Loans

A traditional mortgage option typically used by borrowers with strong credit profiles and a down payment, offered as one of Central Bank’s core home loan choices.

FHA Home Loans

An FHA-backed option aimed at borrowers who want more flexible qualifying guidelines compared to conventional loans.

Jumbo Home Loans

A loan option for higher-priced homes that need financing above standard conventional loan limits.

Low or No Down Payment Home Loans

Central Bank Utah highlights low/no down payment options for borrowers who qualify, including Rural Housing and VA loans with 100% financing.

Mortgage Refinancing

Refinance options for homeowners looking to adjust their payment, change their term, or access equity depending on goals and qualification.

Home Equity Line of Credit (HELOC)

Central Bank Utah includes HELOCs within its personal lending category, offering a revolving line of credit you can draw from as needed. A HELOC is secured by your home’s equity, which is why many people use it for larger planned expenses.

Lot Loans

Lot loans are designed to finance the purchase of land when you’re not ready to build yet. This is a separate product from a construction loan and is meant to hold the lot until construction begins.

Construction Loans

Construction loans are short-term loans used to fund a home build or other real estate construction, typically released in stages as the project progresses. Central Bank positions this as a locally handled option for borrowers working with builders.

Conclusion

Central Bank is a long-standing Utah County community bank with roots dating back to 1891, built around relationship-based service and local decision-making. Across its consumer lineup, it covers the essentials: checking and savings, money market accounts, CDs, a single Visa credit card, and a range of borrowing options including personal loans, auto and recreational lending, and home financing such as mortgages, refinancing, construction and lot loans, and home equity options like a HELOC.

For Utah Valley residents who prefer a local institution with both in-branch support and modern digital access, Central Bank Utah stands out as a stable, established option. As always, verify current rates, terms, and eligibility directly with the bank before opening an account or applying for credit, since details can change over time.

Comparing Options?

Disclaimer:

This page is not affiliated with, maintained by, or sponsored by Central Bank Utah. The information provided in this overview may be outdated or inaccurate after the publication date. UtahFi does not assume responsibility for the accuracy of the content. The logo is a registered trademark of Central Bank Utah.