Bank of Utah: Overview

Bank of Utah was established in 1952 in Ogden, Utah, and its headquarters remain in that city today. Over nearly 70 years, Bank of Utah has expanded across Utah in part through acquisitions, including Bank of Ben Lomond in 1974, followed by Bank of Brigham City and Bank of Northern Utah in 1978—moves that helped broaden its footprint into additional Utah communities.

Bank of Utah is one of the established community banks in the state—if you are comparing options, start with our Best Banks in Utah guide.

Bank of Utah: Corporate Office

2605 Washington Blvd

Ogden, UT 84401

Utah cities where Bank of Utah operates include:

Bountiful, Brigham City, Heber City, Layton, Lehi, Lindon, Logan, Ogden, Orem, Price, Providence, Provo, Roy, Salt Lake City, Sandy, South Ogden, Spanish Fork, St. George, Tremonton.

Expansion

Bank of Utah’s acquisition history shows a clear pattern of expanding within Utah by absorbing smaller community banks and converting them into Bank of Utah branches. Its early growth included the 1974 acquisition/merger of Bank of Ben Lomond, which strengthened its footprint in the Ogden/Weber County area, followed by 1978 acquisitions of Bank of Brigham City and Bank of Northern Utah as it expanded north along the Wasatch Front. In typical community-bank consolidations, offices from the acquired institutions were converted into Bank of Utah locations, helping the bank scale while staying locally rooted.

Later transactions extended that same strategy into additional high-opportunity markets. In 1999, Bank of Utah announced plans to acquire First Commerce Bank, expanding into Cache Valley (Logan) and broadening its reach beyond its original Ogden base, with regulatory approvals appearing in Federal Reserve records around that period. In 2018, Bank of Utah’s holding company (BOU Bancorp, Inc.) completed the purchase of AmBancorp, Inc. (the holding company for American Bank of Commerce / AmBank), a deal that added presence in Utah County (Lindon and Provo) and Wasatch County (Heber)—supporting growth in some of Utah’s fastest-growing communities.

Consumer Products and Services

bankofutah.com | Products and Services

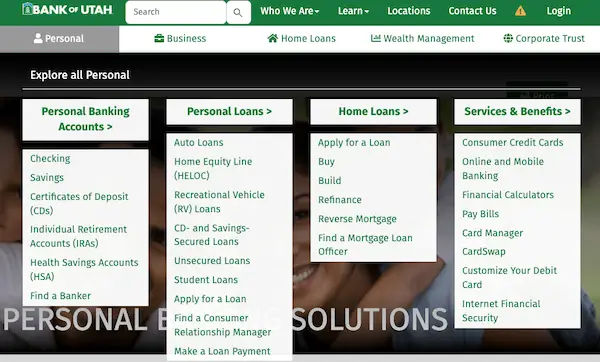

Bank of Utah offers a broad lineup of products and services for both individuals and businesses in Utah, including checking accounts, savings accounts, and CDs. For borrowing needs, it supports common goals like auto loans, unsecured personal loans, secured loans backed by savings or CDs, RV loans, HELOCs, and mortgage options for buying, refinancing, or building.

Beyond everyday banking, Bank of Utah is also widely recognized for Corporate Trust services that serve clients across the U.S., especially aircraft owner trusts. The bank says it is one of the largest providers of aircraft owner trusts in the world, with over 2,000 aircraft held in owner trusts on the FAA registry, plus additional aircraft held through security trusts.

Bank of Utah deposit accounts are FDIC insured up to $250,000 per depositor, per ownership category—see What FDIC insurance means to Utah Bank customers.

Bank of Utah Checking Accounts

Easy Checking

A simple, everyday checking account built for basic banking needs without extra complexity.

- Monthly fee: $0

- Minimum balance requirement: None

- Minimum to open: $100

- Key benefit: straightforward account for routine spending and payments

Read our full Bank of Utah Easy Checking review.

Evergreen Checking

A checking option designed for customers who want a more “premium” experience and long-term stability.

- Monthly fee: $10

- Minimum balance requirement (to avoid fee): $10,000 average monthly balance

- Minimum to open: $100

- Key benefit: positioned for customers who keep higher balances and want a step up from basic checking

Student Checking (Ages 16–26)

A student-focused checking account designed to be easy to use while in school or early in a career.

- Monthly fee: $0

- Minimum balance requirement: None

- Minimum to open: $25

- Key benefit: designed specifically for students ages 16–26

Thrive Checking

A “fresh start” checking account designed for people rebuilding their banking history and re-establishing everyday banking.

- Monthly fee: $0

- Minimum balance requirement: None

- Minimum to open: $5

- Key benefit: eligibility requirement—you can’t owe money to another bank or credit union to open it

For a wider comparison beyond Bank of Utah, use our Best Checking Accounts in Utah guide.

Savings Accounts

Bank of Utah’s savings accounts share a similar day-to-day experience: you can manage them in-branch and digitally, earn interest (based on the account rules), use mobile deposit, track activity in My Money Hub, set up automatic recurring transfers from checking to savings, and use paperless e-statements stored for 7 years.

I Save (Savings)

A general savings account designed for everyday saving goals with a simple setup and standard access to your money. Ideal for balances under $25,000.

- Monthly fee: $0

- Minimum to open: $100

- Minimum balance requirement: None (interest starts at $500)

- Key benefit: tiered savings structure—higher balances can earn higher rates

Children’s I Save

A kids savings account for children under 18 that helps families build saving habits early and transitions automatically later.

- Monthly fee: $0

- Minimum to open: $10

- Minimum balance requirement: None (interest starts at $500)

- Key benefit: automatically converts to I Save when the child turns 18

My Money Market

A money market account designed for customers who want higher earning potential while still keeping access to funds when needed. Ideal for balances over $25,000.

- Monthly fee: $0

- Minimum to open: $100

- Minimum balance requirement: None (interest begins accruing at a $10,000 minimum daily balance)

- Key benefit: 6 free withdrawals/transfers per statement cycle, then a $10 fee per additional debit transaction

Certificates of Deposit (CDs)

Bank of Utah’s CDs are FDIC-insured deposit products, which means your money is protected up to $250,000 per depositor, per FDIC-insured bank, per ownership category (standard FDIC coverage). If you plan to keep more than $250,000 in CDs, Bank of Utah also offers CDARS, which is designed to help customers stay within FDIC insurance limits by spreading deposits across multiple banks while working through Bank of Utah.

3-Month CD

A short-term certificate of deposit designed for savers who want to lock in a guaranteed return for a brief period and keep a near-term timeline.

6-Month CD

A mid-short option that’s often used when you want a little more time than a 3-month term, but still want your money back within the year.

1-Year CD

A classic “set it and forget it” CD term for people saving toward a goal within the next year, with the predictability of a fixed term and rate.

2-Year CD

A longer-term CD option for customers who don’t need immediate access to their funds and want a longer lock-in period.

3-Year CD

A longer-term CD term for more patient savers who want to commit funds for a multi-year goal while keeping the simplicity of a standard CD structure.

Super Saver CD

A CD built for people who want the structure of a traditional CD but still want to keep adding money during the term, which makes it a flexible alternative to standard CDs.

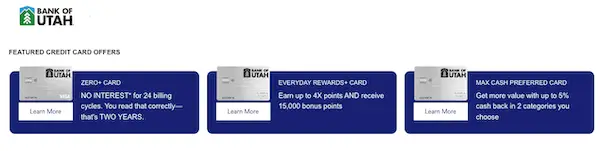

Bank of Utah Credit Cards

Bank of Utah credit cards are built to match different goals—earning rewards, maximizing cash back, saving on interest, or building credit. These cards are issued by Elan Financial Services and offered as Visa credit cards through Elan’s hosted application platform. Welcome bonuses and intro APR offers can change over time, so it’s smart to confirm the current terms during the application process before you apply.

bankofutah.com | Credit Cards issued by Elan Financial Services

ZERO+ Card

Best for people who want a long 0% intro APR but still want cash back.

- Annual fee: $0

- Welcome bonus: Not offered

- Intro offer: 0% intro APR for purchases and balance transfers for 21 billing cycles

- Rewards: 4% cash back on prepaid travel booked in the Travel Center

- Other perks: $15 annual statement credit after 11 consecutive months of purchases, cell phone protection up to $600, and one 3-month $0 ExtendPay Plan offer each calendar year after the intro APR expires

Everyday Rewards+ Card

Best for people who want points for everyday spending and a bonus.

- Annual fee: $0

- Welcome bonus: 25,000 bonus points (worth up to $250) after $1,000 spend in the first 90 days

- Intro offer: 0% intro APR for purchases and balance transfers for 12 billing cycles

- Rewards: 4X points on dining (first $2,000 each quarter), 2X points at grocery stores, gas/EV charging, and eligible streaming, 1X on other eligible purchases

- Other perks: points redemption options vary, with maximum value typically when redeemed to an eligible deposit account

Max Cash Preferred Card

Best for people who want up to 5% cash back in categories they choose.

- Annual fee: $0

- Welcome bonus: $150 bonus after $500 spend in the first 90 days

- Intro offer: 0% intro APR for balance transfers for 12 billing cycles (transfers within 366 days of account opening)

- Rewards: 5% cash back in 2 categories you choose (first $2,000 combined per quarter), 2% unlimited cash back in one everyday category you choose, 1% unlimited on all other eligible purchases

- Other perks: category enrollment required to earn above 1%; cash rewards can be redeemed as statement credit, rewards card, or eligible deposit

Travel Rewards+ Card

Best for people who want travel-focused points plus airport lounge access.

- Annual fee: $0 intro annual fee for the first 12 months, then $99

- Welcome bonus: 25,000 bonus points (worth up to $250) after $2,000 spend in the first 120 days

- Intro offer: Not offered

- Rewards: 4X points on eligible travel, gas/EV charging, entertainment, and recreation; 1.5X points on all other eligible purchases

- Other perks: Priority Pass Select membership for access to 1,700+ lounges and experiences worldwide

Reserve Rewards+ Card

Best for people who want premium rewards and elevated travel perks.

- Annual fee: $390

- Welcome bonus: 50,000 bonus points (worth up to $500) after $4,500 spend in the first 90 days

- Intro offer: Not offered

- Rewards: 6X points on prepaid travel booked in the Travel Center, 2X points on all other eligible purchases

- Other perks: Priority Pass Select membership for access to 1,700+ lounges and experiences worldwide

College Real Rewards Card

Best for students who want to build credit while earning simple rewards.

- Annual fee: $0

- Welcome bonus: 2,500 bonus points (worth up to $25) after your first purchase

- Intro offer: 0% intro APR for purchases and balance transfers for 6 billing cycles

- Rewards: 1.5X points per $1 on all eligible purchases

- Other perks: points can be redeemed for cash back, travel, merchandise, or gift cards (redemption options and values vary)

Max Cash Secured Card

Best for people who want to build/rebuild credit and still earn up to 5% cash back.

- Annual fee: $0

- Welcome bonus: Not offered

- Intro offer: Not offered

- Rewards: 5% cash back in 2 categories you choose (first $2,000 combined per quarter), 2% unlimited in one everyday category you choose, 1% unlimited on all other eligible purchases

- Other perks: Zero Fraud Liability for unauthorized transactions

Secured Card

Best for people who want the simplest secured card to establish or repair credit.

- Annual fee: $0

- Welcome bonus: Not offered

- Intro offer: Not offered

- Rewards: Not offered

- Other perks: Zero Fraud Liability, free credit score access, automatic bill pay, and account alerts.

Business Checking

Bank of Utah offers multiple business checking accounts designed for different types of organizations—from small businesses that want a simple setup to larger companies that need more structure and treasury support. Across the lineup, these accounts are built around transaction flexibility, local support, and access to cash management tools for Utah-based businesses.

Free Business Checking

A business checking option designed for lower transaction volume and straightforward day-to-day needs.

Read the full review of Free Business Checking account.

Analyzed Business Checking

A business checking account built for higher transaction activity, where pricing is typically tied to usage and treasury services.

Business Advantage Checking

A business checking option designed for sole proprietors who want a checking account that can earn interest on balances.

Non-profit Advantage

A business checking option built for nonprofits that want an interest-earning account structured to keep ongoing costs low.

Public Fund Advantage

A business checking option designed for public entities that want interest earnings while keeping fees minimal.

These accounts vary by structure—especially around transaction activity, service features, and interest—while staying supported by digital banking tools, payment services, and in-branch access.

Consumer and Personal Loans

bankofutah.com | Loans

Bank of Utah groups its personal borrowing options under Consumer & Personal Loans, with applications handled through an online loan application and supported by local loan officers.

Auto Loans

Financing designed for new or used vehicles, including options to refinance or access vehicle equity.

- Loan type: secured by the vehicle

- Common uses: purchase, refinance, lower payment, or cash-out (where available)

- Key benefit: built specifically for vehicle financing (not a general-purpose loan)

- Good to know: approval and terms typically depend on credit, income, and vehicle details

Home Equity Line of Credit (HELOC)

A revolving credit line that lets you borrow against your home’s equity for flexible spending needs.

- Loan type: secured by your home

- Common uses: renovations, debt payoff, major expenses

- Key benefit: revolving access—borrow, repay, and borrow again (within limits)

- Good to know: rates and limits typically depend on credit and available equity

Recreational Vehicle (RV) Loans

Loans for a wide range of recreational vehicles, with options that may include refinance and equity access.

- Loan type: secured by the RV (or recreational asset)

- Common uses: motorhomes, trailers, boats, motorcycles, ATVs, snowmobiles

- Key benefit: designed for “toys” and recreation financing, not just autos

- Good to know: terms can vary based on the type of vehicle and collateral

CD- and Savings-Secured Loans

A secured loan that uses your CD or savings as collateral while keeping your deposit intact.

- Loan type: secured by your deposit account

- Common uses: credit-building, planned expenses, access to cash without selling savings

- Key benefit: your deposit can continue earning interest during the loan term

- Good to know: borrowing limits are typically tied to your deposit amount

Unsecured Loans

A personal loan that doesn’t require collateral and can be used for a wide range of needs.

- Loan type: unsecured (no collateral)

- Common uses: purchases, unexpected expenses, debt consolidation

- Key benefit: flexible use of funds without pledging an asset

- Good to know: approval and pricing are based mainly on credit, income, and overall profile

Student Loans

Student lending offered through Bank of Utah’s partnership with College Ave, covering multiple education paths.

- Loan type: education-focused lending

- Common uses: undergraduate, graduate, parent loans, and refinancing

- Key benefit: built specifically around education funding and repayment scenarios

- Good to know: terms and eligibility depend on program type and borrower/co-signer profile

Mortgages & Home Loans

Bank of Utah’s home loan options cover the most common paths to homeownership and home equity—from buying and refinancing to building, purchasing land, and tapping equity for flexibility.

Purchase & Refinance

Mortgages designed to help you buy a home or refinance an existing one, with options meant to match different borrower needs and timelines.

Construction Loans

Loans for building a new home, typically structured around the construction timeline and draw process, and often available for contractor-built projects (and sometimes owner-builders).

Lot Loans

Financing for an improved lot when you plan to build a primary residence on the land within the loan term.

HELOC

A home equity line of credit that uses your home’s equity to provide a revolving credit line for renovations, major expenses, or added flexibility over time.

Reverse Mortgage (HECM)

A reverse mortgage option for eligible homeowners designed to convert home equity into funds, commonly used to refinance or support a home purchase later in life.

Investments & Wealth Management

Bank of Utah’s investments offering sits inside its broader Wealth Management group and follows two tracks: investment management (how your money is invested) and trust/fiduciary administration (how assets are managed and distributed under legal instructions). Their trust team emphasizes objectivity and fiduciary standards, meaning they administer trusts based on the trust terms and required guidelines, while also handling operational needs like record-keeping and assistance with tax preparation.

On the investment side, Bank of Utah offers investment management solutions and highlights self-directed IRA opportunities for clients who want more control over their retirement holdings. Their approach is positioned as collaborative, with private bankers and trust officers working together to build a plan around goals like retirement planning and legacy planning. Non-deposit investment products are not FDIC insured.

Conclusion

Bank of Utah is a long-standing Utah institution founded in 1952 and headquartered in Ogden, with decades of growth shaped in part by acquisitions such as Bank of Ben Lomond (1974), Bank of Brigham City and Bank of Northern Utah (1978), First Commerce Bank (1999), and American Bank of Commerce/AmBank (2018). That history reflects a bank that has expanded into key Utah communities while maintaining a strong local foundation.

Today, Bank of Utah offers a full range of products and services—from checking, savings, CDs, credit cards, and consumer loans to home lending options like purchase/refinance, construction loans, lot loans, HELOCs, and reverse mortgages. Beyond traditional banking, it’s also recognized nationally for corporate trust services, and it provides wealth management and trust services for clients focused on investing, retirement planning, and legacy planning.

COMPARING OPTIONS?

Disclaimer:

This page is not affiliated with, maintained by, or sponsored by Bank of Utah. The information provided in this overview may be outdated or inaccurate after the publication date. UtahFi does not assume responsibility for the accuracy of the content. The logo is a registered trademark of Bank of Utah.