Bluevine: Overview

![]() Bluevine is a fintech company focused on business banking rather than traditional branch-based consumer banking. Bluevine is best understood as a digital-first option for small businesses that want online checking, payment tools, and access to working capital, not as a local Utah bank with a statewide branch network. Bluevine says it was founded in 2013 to build better banking solutions for small and midsize businesses, and its current platform centers on business checking with lower fees, money movement tools, and access to credit.

Bluevine is a fintech company focused on business banking rather than traditional branch-based consumer banking. Bluevine is best understood as a digital-first option for small businesses that want online checking, payment tools, and access to working capital, not as a local Utah bank with a statewide branch network. Bluevine says it was founded in 2013 to build better banking solutions for small and midsize businesses, and its current platform centers on business checking with lower fees, money movement tools, and access to credit.

Background and Growth

Bluevine was founded in 2013 by Eyal Lifshitz and Nir Klar, and it has grown from a small business financing company into a broader digital banking platform for businesses. The company now lists Jersey City, New Jersey, as its official headquarters, and also includes operations in Cottonwood Heights, Utah. From a Utah perspective, that gives Bluevine some relevance in the state, even though it is not a Utah community bank with a local branch network.

What Bluevine Does

Bluevine provides digital financial tools for small businesses through an online platform built around business checking, payments, and access to credit, which is why it is generally considered a fintech rather than a traditional bank. Its banking services are provided by Coastal Community Bank, Member FDIC, while Bluevine delivers the digital platform and business tools around that relationship.

For business owners in Utah, Bluevine is best understood as a digital-first option for small businesses that want online checking, payment tools, and access to working capital rather than a local bank with a statewide branch network.

Read our What FDIC Insurance Mean for Utah Bank Customers guide.

Main Products and Services

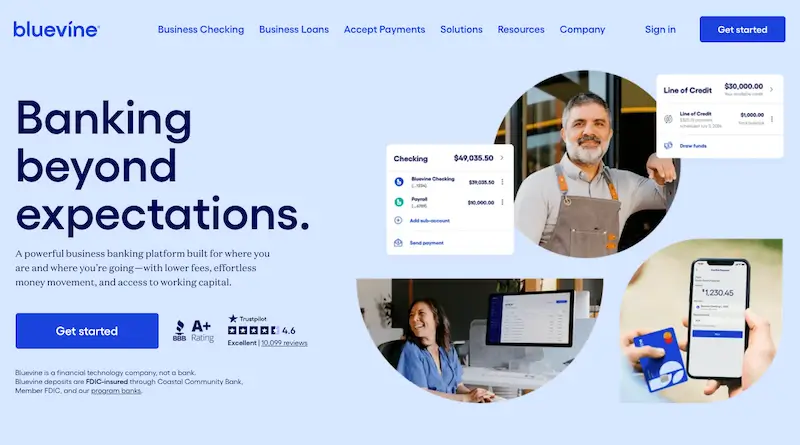

bluevine.com | Homepage

Bluevine’s main products and services are built around business banking rather than personal finance. Its platform focuses on a small number of core business tools instead of a broad menu of traditional consumer banking products.

- Business Checking: Digital business checking designed for day-to-day banking.

Bluevine Business Checking is included in our list of the best business checking accounts in Utah.

- Payments and Money Movement: Tools for sending, receiving, and managing business payments

- Business Line of Credit: Working capital access for eligible businesses

Platform, Access, and Requirements

Bluevine is built as a digital-first business banking platform, and its mobile app is part of that experience rather than a separate product.

This reflects the broader shift toward digital-first banking, where financial services are accessed primarily through apps and online platforms. For a deeper explanation, see Digital-First Banking: How Online Platforms Are Changing. Bluevine says businesses can manage cash flow, pay bills, track transactions, and deposit checks from the Bluevine app, while its broader platform also supports online account access, payments, and account management through the web.

Access is geared toward U.S. businesses that want to handle everyday banking tasks online instead of through branches. Bluevine also says its platform includes tools such as mobile check deposit, financial app connections, and account access features for accountants and bookkeepers, which helps reinforce its focus on digital business operations.

At the same time, businesses still need to pay attention to eligibility rules, fees, and product requirements. Bluevine promotes low-fee business checking, but certain services can still carry fees, and qualification standards can apply for products such as its line of credit.

Bluevine app icon

![]()

App Store rating: 4.7 of 5. 4k ratings

Who It Serves Best

Bluevine is best suited for small businesses that want a digital banking option with core operating tools in 1 place. It can make the most sense for business owners who value online account access, streamlined payments, and potential access to working capital more than in-person branch service. Its overall setup is especially relevant for startups, freelancers with formal business entities, online businesses, and other companies that prefer speed, convenience, and digital account management.

Limitations

Bluevine is not a bank, which means its banking services depend on partner institutions. Bluevine says its banking services are provided by Coastal Community Bank, Member FDIC, and that deposits are placed through Coastal Community Bank and program banks. That structure can work well for customers, but it also means Bluevine depends on outside banking partners rather than controlling those banking functions directly. From a practical standpoint, partner changes could affect how services are structured over time, which is a limitation compared with a traditional bank that holds deposits under its own charter.

Read our guides for Best Banks in Utah and Best Credit Unions in Utah.

Conclusion

Bluevine is best understood as a business-focused fintech rather than a traditional bank. It has grown from a small business financing company into a broader digital platform centered on business checking, payments, and access to credit. While its banking services are provided through Coastal Community Bank rather than under Bluevine’s own bank charter, its overall model may still appeal to businesses that want speed, convenience, and digital money-management tools in 1 place. From a Utah perspective, Bluevine stands out more as a modern business banking option with some relevance to the state than as a local institution with a branch-based presence.

COMPARING OPTIONS?

Disclaimer:

This page is not affiliated with, maintained by, or sponsored by Bluevine. The information provided in this overview may be outdated or inaccurate after the publication date. UtahFi does not assume responsibility for the accuracy of the content. The logo is a registered trademark of Bluevine, Inc.