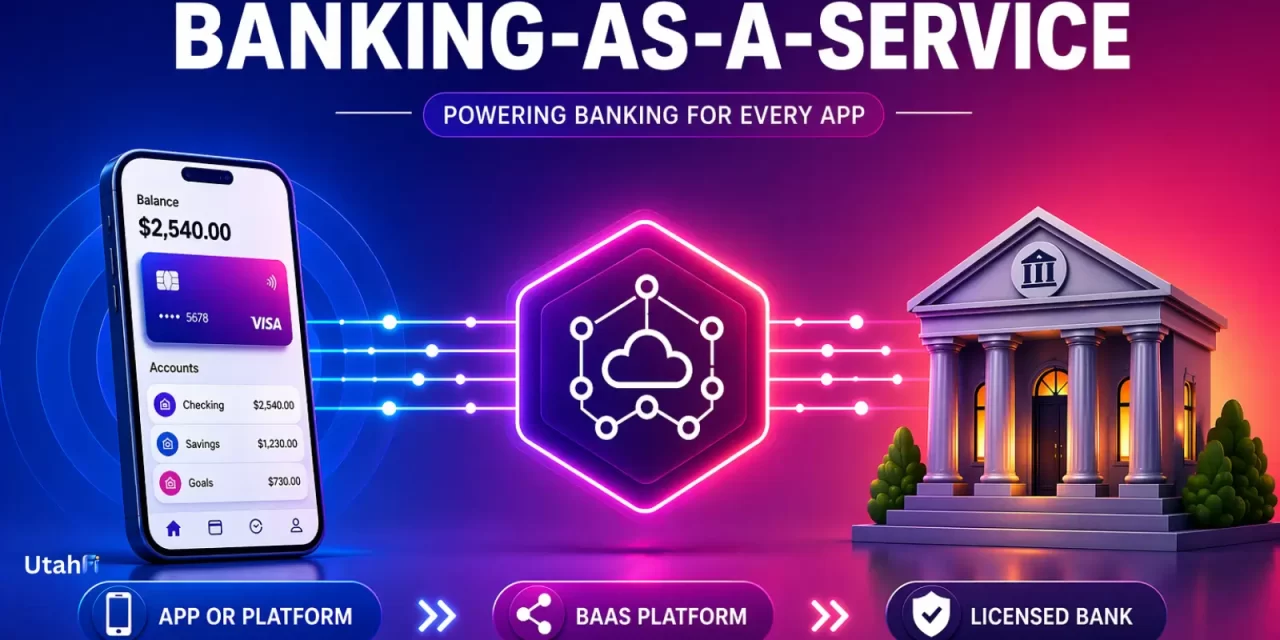

What Is Banking-as-a-Service (BaaS)

Banking as a service (BaaS) is a model that allows companies to offer banking features without being banks.

Instead of building a bank from scratch, a company can connect to a licensed financial institution and use its infrastructure to provide services like accounts, cards, payments, and money movement.

In this setup, the bank operates in the background, handling regulation, compliance, and holding customer funds, while the company controls the app or platform that people interact with.

This shift means that banking is no longer limited to banks. Financial services can now be built into apps, platforms, and digital products across many industries.

In Simple Terms

Banking as a service means a company can offer banking features without being a bank.

Instead of creating a bank, the company uses a licensed bank behind the scenes and focuses on the app or service you use.

For example, an app can give you a card or an account, but the money is actually held by a real bank working in the background.

You use the app, but the bank powers it.

What Changed (Before vs Now)

In the past, only banks could offer banking services. If you wanted an account, a card, or a way to move money, you had to go directly to a bank.

Banks controlled everything:

- Accounts

- Cards

- Payments

- Customer relationships

This created a system where financial services were centralized inside banks, with limited flexibility and slower innovation.

Today, that model is changing.

With banking as a service, companies can build financial features into their own products by connecting to a licensed bank through modern infrastructure.

Instead of everything happening inside a bank:

- Apps and platforms create the user experience

- Infrastructure connects systems

- Banks handle regulation and hold funds

The shift is from a bank-controlled system to a platform-powered model, where financial services can exist inside apps, software, and digital platforms.

Traditional Banking vs Banking as a Service

Examples of BaaS

Banking as a service is already part of many everyday financial experiences, even if it is not always visible.

Common examples include:

- Apps offering debit cards linked to user accounts

- Platforms offering accounts inside their ecosystem

- Marketplaces enabling payments and transfers between users

- Business tools integrating payments, payroll, and financial workflows

A clear real-world structure can be seen with a fintech app like Chime, which offers accounts and debit cards by working with sponsor banks such as The Bancorp Bank and Stride Bank, where customer funds are held and protected through deposit insurance provided by the Federal Deposit Insurance Corporation.

Infrastructure providers like Galileo Financial Technologies connect the systems and enable the service to function.

This structure shows how apps, infrastructure, and banks work together.

How Banking-as-a-Service Works

Banking as a service works by separating banking into different layers, with each one handling a specific role.

- Licensed banks hold deposits, manage compliance, and operate under financial regulations, including providing FDIC insurance for customer funds

- Infrastructure providers connect systems through APIs, allowing platforms to access banking functions like account creation, card issuing, and payments

- Platforms and apps build the user experience, creating the interface that customers interact with

This structure allows companies to offer banking features without becoming banks.

Instead of building everything from scratch, a company can:

- Connect to a licensed bank

- Use infrastructure to access banking capabilities

- Focus on building a better product for users

The result is a system where banking becomes a service that can be integrated into almost any app or platform.

This type of infrastructure also supports lending products, where loan management systems handle what happens after a loan is issued, as explained in Loan Management Systems Powering Modern Lending Platforms.

Key Players and Competitors

Banking as a service is powered by infrastructure companies that connect apps to licensed banks, making it possible to launch financial products without becoming a bank.

A key company connected to this model in Utah is Galileo Financial Technologies, which provides APIs and financial infrastructure used by fintechs and digital platforms.

Other companies operating in this space include:

- Stripe (Treasury), which offers banking capabilities to businesses through its platform

- Unit, which helps companies launch financial products by connecting them to partner banks

- Treasury Prime, which provides APIs for account creation, payments, and bank integrations

- Solaris, which operates a similar model in Europe

These companies play a central role in enabling platform-based banking, allowing apps and businesses to offer financial services without becoming banks themselves.

Why It Matters

Banking as a service is changing how financial services are created and delivered.

Instead of relying only on banks, companies can now build financial features directly into their products, creating new types of experiences for users.

This shift leads to:

- Faster innovation, as companies can launch financial features more quickly

- More competition, as new players enter the market

- More tailored products, designed for specific industries and use cases

- Lower barriers to entry, reducing the need to build a bank from scratch

For users, this means that banking becomes more accessible and integrated into everyday tools.

Instead of going to a bank for every financial need, people can manage money inside the apps and platforms they already use, reflecting the shift toward digital-first banking experiences. For a deeper explanation, see Digital-First Banking: How Online Platforms Are Changing.

This is turning banking from a destination into a built-in feature of digital experiences.

BaaS and Embedded Finance

Banking as a service is closely connected to embedded finance, which is explained in Embedded Finance: How Financial Services Are Moving Inside Apps.

Embedded finance is the user-facing result, while BaaS is part of the infrastructure behind it.

BaaS makes it possible for companies to:

- Add accounts, cards, and payments to their products

- Integrate financial features directly into apps

- Deliver financial services without becoming banks

In other words, embedded finance is what users see, and banking as a service is what makes it possible behind the scenes.

BaaS and Open Finance

Banking as a service is also connected to open finance, which is explained in Open Finance: How Financial Data Becomes Shareable and Portable.

While BaaS focuses on delivering financial services, open finance focuses on sharing financial data across platforms.

Together, they enable:

- Connected financial experiences, where data and services move between apps

- More personalized products, built using real financial information

- Greater flexibility, allowing users to access services across different platforms

In simple terms, open finance allows data to move, and banking as a service allows services to be delivered.

Limitations

Banking as a service introduces new possibilities, but it also comes with tradeoffs.

- Dependence on partner banks, since companies rely on licensed banks to hold funds and handle compliance

- Regulatory complexity, as financial services must follow strict rules across different jurisdictions

- Reliance on third-party infrastructure, which can create dependencies on external providers

- Operational risks, especially when multiple systems and integrations are involved

These factors mean that while BaaS makes it easier to build financial products, it also requires coordination between multiple parties.

In many cases, companies are not fully in control of the entire system, which can affect speed, flexibility, and risk management.

What’s Next (Future of BaaS)

Banking as a service is still evolving, and its role in financial services is expected to expand.

Several trends are shaping what comes next:

- More companies offering banking features, as financial tools become part of everyday products

- Deeper integration into apps and platforms, making banking more seamless and less visible

- Global expansion, as infrastructure and regulations develop across different markets

- Convergence with AI and data systems, as explained in AI in Finance: How Artificial Intelligence Is Changing Money, enabling more automated and personalized financial experiences

Over time, banking is likely to become even more embedded into digital experiences, where users interact with financial services without needing to go to a traditional bank.

This points toward a future where banking is not a place, but a capability that exists across platforms and industries.

Conclusion

Banking as a service represents a major shift in how financial services are built and delivered.

What used to be controlled entirely by banks is now distributed across platforms, infrastructure providers, and licensed banks, allowing companies to offer financial features without becoming banks themselves.

This change is not just technical. It is redefining who can offer banking and where financial services appear.

As a result, banking is becoming:

- More accessible, reaching users through the apps they already use

- More integrated, embedded into everyday digital experiences

- More flexible, adapting to different industries and use cases

Banking is no longer just something people go to. It is becoming something that is built into the products and services they use every day.

Disclaimer: Information in this article is for educational purposes and may change over time.