Introduction

Understanding simple interest vs compound interest is important because these two concepts affect how money grows in savings and investments and how interest builds up on loans.

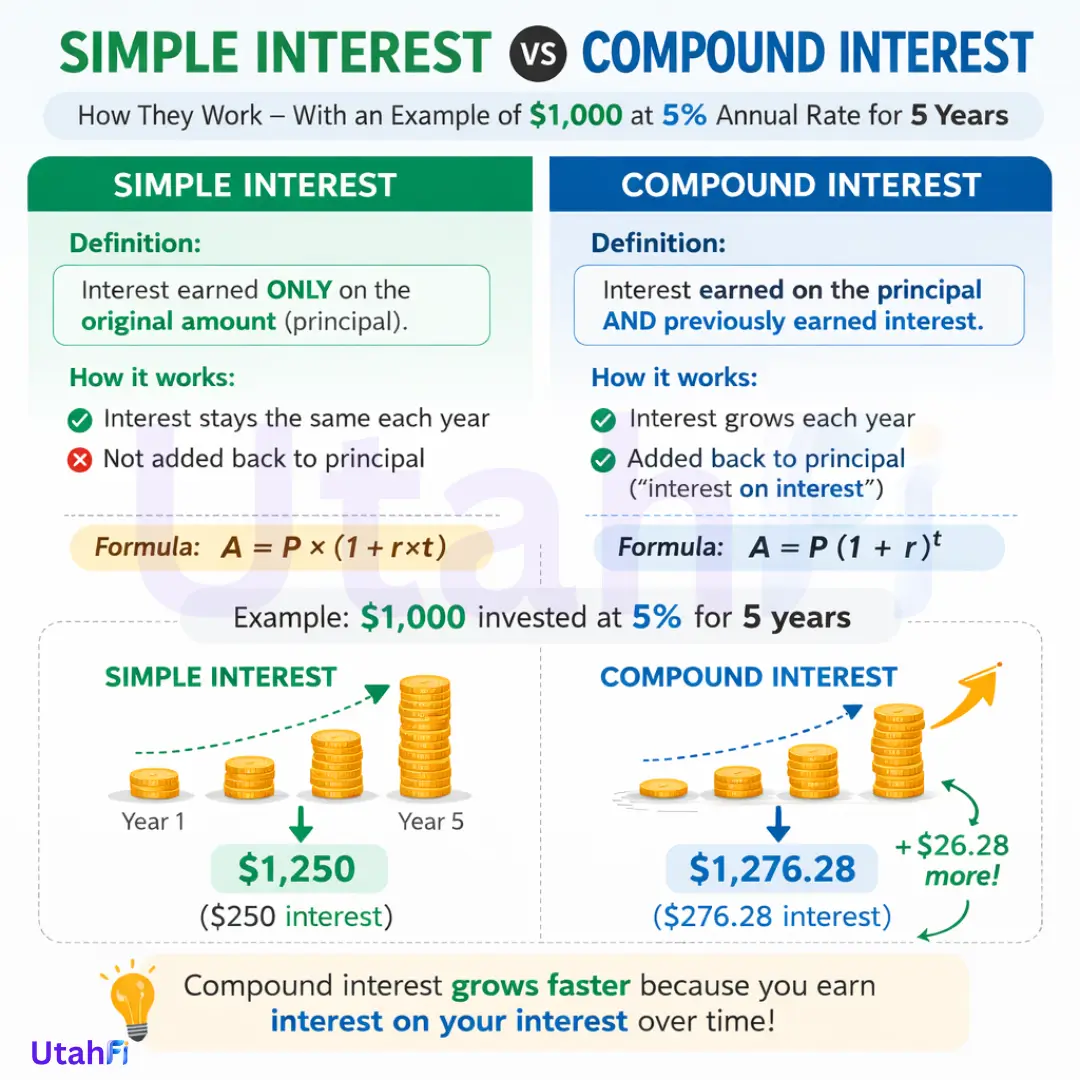

Simple interest is calculated only on the original principal, while compound interest is calculated on both the original principal and the previously earned interest.

Over time, that difference can have a major impact on how much you earn from savings or investing, or how much you pay when borrowing money.

What Is Simple Interest?

Simple interest is calculated only on the original principal, which is the amount of money initially deposited, invested, or borrowed.

The basic formula is:

Interest = Principal × Rate × Time

For example, if you put $1,000 into an account that earns 5% simple interest per year, you would earn $50 per year in interest.

After 5 years, the total interest earned would be $250, because the interest is always calculated only on the original $1,000.

This makes simple interest easy to understand and predictable, but it usually does not grow as quickly as compound interest over longer periods.

What Is Compound Interest?

Compound interest is calculated on both the original principal and the interest that has already been earned.

That means interest begins to earn interest on itself over time, which can accelerate growth.

For example, if you deposit $1,000 into an account that earns 5% compound interest, the interest earned in the first year is added to the balance. In the second year, interest is calculated on that new, larger balance instead of only on the original amount.

Because of this compounding effect, money can grow faster the longer it stays in the account or investment.

Why Compound Interest Matters

Compound interest can make a major difference in long-term saving and investing.

When growth compounds over time, even small contributions and modest returns can produce much larger balances than many people expect. The longer the timeline, the more powerful compounding becomes.

This is one reason it often helps to start saving early. Time gives compound interest more opportunity to work, which can lead to stronger long-term results.

You can also use the Rule of 72 as a quick way to estimate how long it may take money to double at a given interest rate.

Read our article What is the Rule of 72? to learn more about it.

Simple Interest vs Compound Interest Example

A side-by-side example can make the difference easier to see.

Suppose you deposit $1,000 at an annual interest rate of 5% for 5 years.

With simple interest, you earn $50 each year because the interest is always based only on the original $1,000. After 5 years, you would earn $250 in total interest, giving you a final balance of $1,250.

With compound interest, the interest is added to the balance each year, so the next year’s interest is calculated on a slightly larger amount. After 5 years, the balance would grow to about $1,276.28.

The difference may look small in a short example, but over a much longer time period, compound interest can pull much further ahead.

Where You See Simple Interest vs Compound Interest

Both types of interest appear in everyday financial products, but they are not used in the same way.

Simple interest is commonly found in:

- some personal loans

- certain short-term lending products

- some auto loans

Compound interest is more common in:

- savings accounts

- money market accounts

- investment accounts

- credit cards

- many long-term financial products

Understanding which type of interest applies can help you compare financial products more clearly and make better financial decisions.

For official consumer education on compounding, you can reference the U.S. Securities and Exchange Commission’s Compound Interest Calculator.

Final thoughts

The difference between simple interest and compound interest may seem small at first, but over time it can create very different financial outcomes.

Simple interest grows at a steady and predictable rate, while compound interest allows money to grow faster because returns build on previous returns.

Understanding simple interest vs compound interest can help you make better decisions when choosing savings accounts, evaluating loans, or planning long-term financial goals.